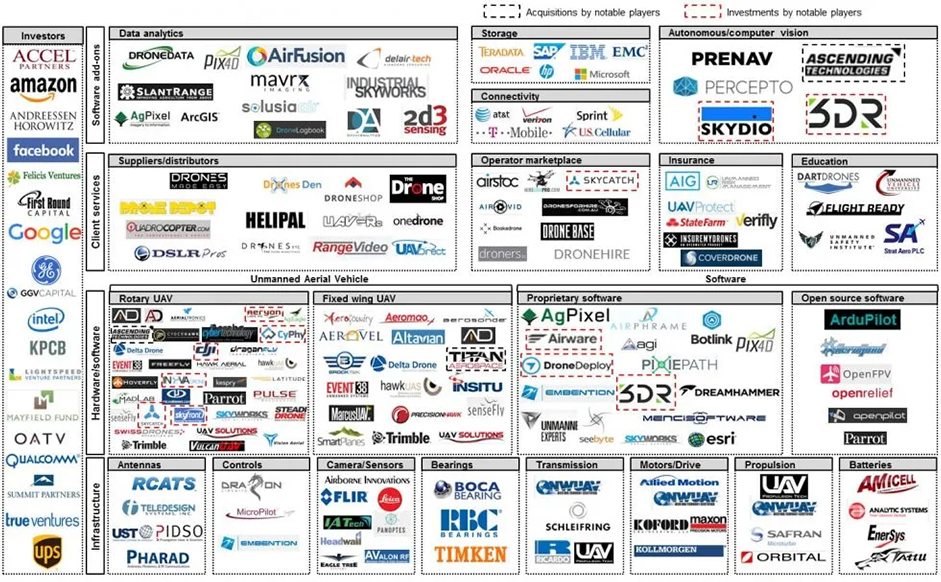

Advances in commercial UAV technology (commercial drones) have rapidly unlocked new applications from precision agriculture to infrastructure surveillance as the prospect of significant revenue pools, enhanced business models, and market extensions have attracted a variety of industrial and financial players who are seeking footholds in the drone ecosystem with aspirations to lead and innovate – or simply hedge.

The resulting fragmented ecosystem consists of a diverse set of market participants ranging from historically upstream chipset vendors to downstream services vendors such as P&C insurers. See Exhibit 1. Naturally, investors are confronted with a problematic proposition: who will succeed in the burgeoning and progressively complex drone ecosystem?

Exhibit 1: The Commercial Drone (UAV) Market Map

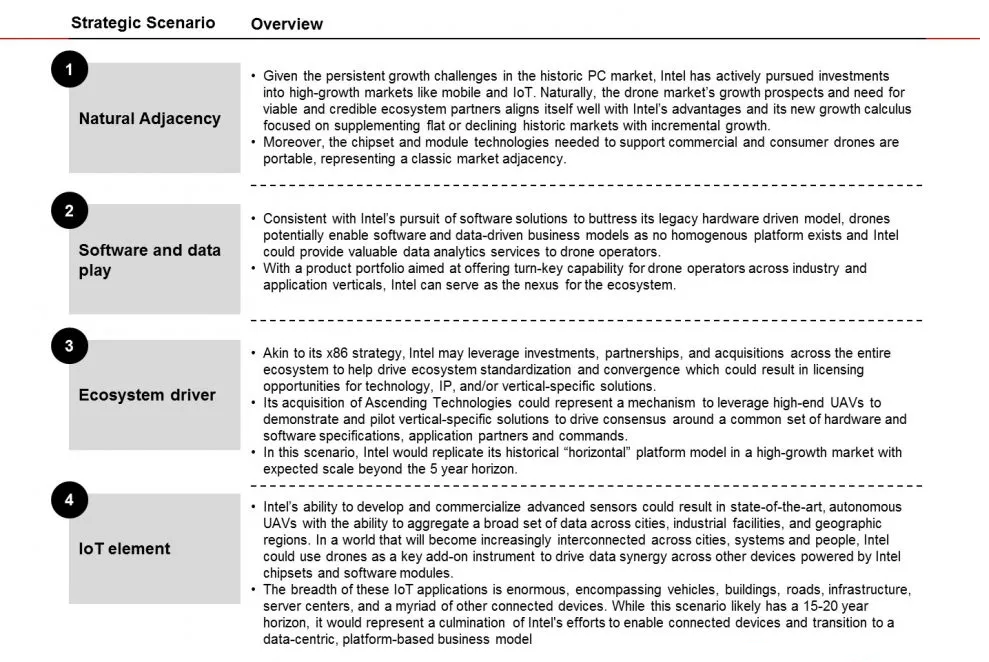

One Leading Investor

One player that has garnered attention due to its multitude of investments across the value chain is Intel – we believe Intel’s minority investments (Airware, Yuneec), partnerships, and acquisitions (Ascending Technologies) across platform OS/software, drone hardware, and data analytics afford it with a unique position in the ecosystem. This unique position will allow Intel to potentially pursue one of several new initiatives and business strategies in the next 5-10 years, in ascending order of strategic and market impact (See Exhibit 2):

- Natural adjacency

- Software and data play

- Ecosystem driver

- IoT element

Exhibit 2: Potential Strategic Models for Intel

Other Notable Entrants

While Intel has been exceptionally active through a wide scope / scale strategy, other players are eager to pursue the frontier landscape of drone technology ranging from those with commercial and operational objectives like General Electric and UPS, to companies tied to technological advancement and product integration like Google, Facebook, Amazon, and Qualcomm.

Strategies have varied by player but the aggregate trend across top investors indicates a concentration of activity in the rotary UAV and proprietary software segments of the ecosystem – this implies a necessity for developing core segments of the drone value chain before expanding into value added segments such as data analytics and drone insurance software.

As an outlier, Facebook, pursued a core drone player through the acquisition of fixed wing UAV manufacturer Titan Aerospace for $60M, likely with the objective of utilizing drones as an infrastructure element to maintain connectivity for the controversial “Internet.org” project.

Qualcomm deviates from general trend in that while the majority of investors have made large scale acquisitions of prominent drone players, Qualcomm has kept its investments relatively small – but with higher frequency – funding approximately ten players, with major drone players like 3DR pulling in the most cash.

While the ecosystem continues to develop, ancillary players (Insurance Carriers, Mobile Network Operators, Data Analytics Platforms, and Data Storage Vendors) will need to monitor the ecosystem to answer strategic questions with clarity:

Issues to note:

- How will the ecosystem evolve to adjust for vertical specific solutions across key markets?

- How will end-customers deploy UAV technology to enhance value propositions

- What business models will succeed for ancillary players given the near-term fragmentation?

- When will profit pools solidify and across which discrete segments of the value chain?

- Which major operating companies are best positioned to drive value through UAV data?