ABSTRACT: Under pressure from depressed oil prices, increased competition and viable alternatives, oil operators have struggled to weather an unprecedented industry downturn. With an uncertain outlook for future oil prices, exploration of new oilfields has become uneconomical in many circumstances and oil companies have instead turned towards digital solutions as a way to optimize their current operations. This set of solutions has been grouped together and termed the “digital oilfield”, with capabilities such as integrated asset management, optimization of processes through data analytics and automation of oilfield assets. Adoption of these solutions will have diverse impacts on different types of oil operators, from the major IOCs and NOCs to smaller independent operators and oilfield services companies.

Digitization and the Oilfield

The advent of the Information Age has been transformative – industry after industry, ranging from law, media, and manufacturing have changed value propositions, business models and operating practices to adapt to the paradigm shift. Traditionally, the oil and gas industry has been on the cutting edge of technology, rapidly adopting new technologies to enable optimal economic recovery of oilfields. However, the “Age of Data” has yet to be realized, as the transformational effects from applying digital technology in other industries has not been realized within the oil and gas industry.

There are several reasons for the delayed adoption of digital technologies in the O&G industry.

A Brief Recap of O&G History

In the mid-20th century, finding oil reserves was easy and the post-WWII economic boom created a large population with voracious demand. Global operators focused on finding new oilfields and commencing drilling rapidly, ensuring a steady supply and reserve of oil – efficiency was typically relegated to a secondary afterthought. Massive oilfields in the Middle East, China and Mexico were discovered, promising a substantial bounty to those who discovered them and made oil companies prioritize the discovery – not efficient extraction – of new oilfields. The O&G industry reached “peak oil” discoveries in the 1960s and incremental yearly oil discoveries have been declining since – however, a cutback in oil consumption due to the oil shock in 1970s and the sheer size of previously discovered oilfields masked the need for companies to extract oil more efficiently.

Operations and digitization challenges

Additionally, the O&G upstream production and exploration process is a complex, multi-faceted task with a number of distinct players across many industries. Unlocking the full value of a digitized oilfield would require an integrated digital platform that necessitates coordination and adoption of digital solutions throughout the O&G value chain. A full digital integration of the O&G value chain demands a large capital investment – given the recent downturn, many operators view this investment prohibitive, preferring a risk-sharing model with other value chain partners.

With recovery from the downturn potentially slowed or delayed, combined with shifting competitive dynamics in the upstream O&G space, operators have begun to build towards the “digital oilfield” in earnest as they pull back from exploration and discovery and shift to a mentality that favors a maximization of fields already in use.

Accelerating Implementation of the Digital Oilfield

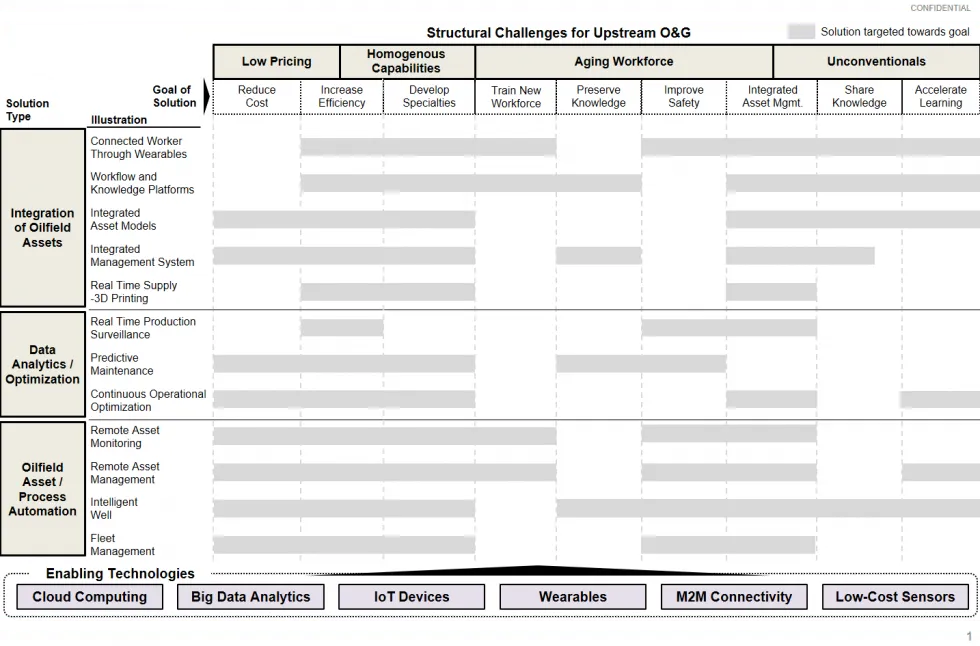

There are several macro drivers that are expected to catalyze adoption of the digital oilfield, including persistently low oil prices, homogenizing E&P capabilities, the continued growth of unconventional, off-shore reservoirs, and an aging workforce. (See Exhibit 1)

Exhibit 1 – The Digital Oilfield Address Industry Challenges

Many industry analysts expect oil prices to remain depressed for the near future, which has a direct impact on investment within Upstream O&G. Industry discussions with operators have revealed that many are still operating on a month-to-month budget, with major investments in exploration significantly delayed or cancelled altogether. Rather, many operators are shifting their focus on maximizing production from existing oilfields. Operators are now feeling an increasing need to reduce costs and streamline production processes, as depressed oil prices place pressure on margins and render new exploration economically unviable. Digital oilfield technologies can assist operators through production optimization by identifying underdeveloped fields, reducing waste, and maintaining asset health, among other process improvements.

Another catalyst in digital oilfield implementation is the need for operators to develop competitive advantages / differentiation as oil company capabilities become increasingly similar. While there will always be areas where specific operators have an advantage (e.g., Halliburton in the shale space), developing an end-to-end digitized solution provides players with a competitive differentiator as both major independents and state oil companies have tried to develop capabilities similar to major IOCs. Among the major IOCs, the services offered have become increasingly similar and with current commodity pricing, operators have redoubled efforts to improve efficiency and reduce costs, much of which is enabled through adoption and rollout of digital oilfield technologies.

As conventional onshore oilfields reach depletion and new fields become increasingly difficult to discover, the era of “easy oil” has come to a close and focus has shifted to offshore and unconventionals as the next wave of oil reserves. Compared to conventionals, unconventional fields not only encompass a wider range of disparate geographies, but also require a larger number of well drillings and a more complex decision set, requiring large amounts of data and analytics to develop optimized processes. Advancements in sensor technology, wireless communication, and Big Data analytics have rendered these processes manageable, and operators are taking advantage through adoption of related digital oilfield technologies.

Another trend operators have to deal with is an aging workforce and an unprepared new talent pool. The traditional background for many upstream employees has been geophysics, geology or other specialized petroleum engineering focused fields. As this portion of the workforce retires, operators have noted a clear disparity in industry preparedness. This has placed an increasing focus on knowledge management and ensuing institutional memory to ensure continued smooth operation and retention of critical knowledge, in light of these gaps. New software leveraging advanced algorithms and Big Data analytics based on the knowledge base of the traditional workforce removes some of the burden by automating and optimizing processes based on mountains of historical data, effectively eliminating the threat of lost knowledge.

Digital Oilfields counteract industry trends

The underlying principles / goals of the digital oilfield are to improve operational efficiency and increase profitability through the implementation of an integrated, end-to-end digital workflow. A combination of modern business process management practices, advanced communication capabilities and deep analytics proficiencies allow operators to streamline processes and disrupt the traditional operating model in order to restructure it into a more efficient model.

Integration of infrastructure, processes and people lies at the core of the digital oilfield. Corporate level complexity at traditional IOCs make information-sharing and decision-making a difficult and time-consuming tasks. For example, many operators are organized at the silo level, which typically encompass specific corporate functions or regional offices. Within these siloes, each exercises a relatively high level of independence, which can fluctuate based on corporate culture. While data and knowledge travels relatively efficiently through each silo, cross-silo communication and transfer of insight is limited, resulting in uncoordinated adoption of innovative processes and practices – thus capping potential operational improvement.

Two Examples

Digital oilfield solutions span a diverse set of applications and providers and are built upon / enabled by IoT infrastructure. (See Exhibit 2)

Exhibit 2 – The Digital Oilfield Ecosystem (Not Exhaustive)

Currently, many digital oilfield companies focus on creating a platform that enable cross-functional and cross-company coordination. For example, Maana, a data analytics firm, has partnered with Shell and Chevron to develop a digital knowledge platform that collects data from sources across the company and applies Big Data analysis to develop and operationalize insights. In unconventional drilling situations, this materializes as a comprehensive, real-time view of well data such as rig sensor data, downhole log files, and proprietary databases. This data is then aggregated and presented to well engineers, which allows them to optimize well-planning and drilling. The solution leverages machine learning capabilities to continually refine the insights provided and allows for easy communication of information to all users, regardless of location and function.

Another example is Parsable, a software company founded by former Google and Microsoft executives and backed by Schlumberger, Saudi Aramco, and Airbus, among others. Parsable has created a platform that combines communication, data collection, performance tracking and analytics into a single package for rapid communication between frontline and back office employees. It aims to transform the production process by digitally organizing work, fostering real-time collaboration, and providing analytics to drive improvement. The platform captures and transmits field data from “Internet of Things” devices with rich media such as pictures and videos, allowing workers to collaborate with experts and supervisors in real time. New employees can use the platform for immediate responses to requests for guidance, reducing training time and improving worker safety. Notifications are sent to relevant parties in real-time, reducing turnaround for maintenance and lowering downtime. A knowledge-base can be built up and easily distributed across the company, accelerating adoption of innovative practices.

Big Data analysis and automation

Once a process is integrated into a digital oilfield platform, additional analysis can be conducted to optimize them (e.g., finding chokepoints that prolong process, eliminating redundant steps). Big Data analytics combined with cloud computing power revives historical data, uncovering insights that were difficult to spot beforehand. Data-driven insights can speed up the decision-making process and avoid errors due to subjective judgement, limited information or incorrect interpretation of data. Big Data analytics also allows operators to be proactive with solutions such as predictive maintenance, where data from assets is used to recognize patterns in reliability and performance and develop maintenance patterns that address problems before they occur. In unconventional oilfields, operational data can be analyzed to rapidly update best practices, increasing efficiency.

Automation of simple, repetitive tasks is also possible in a digital oilfield. Enabled by M2M communication and edge-level intelligence, tasks that do not require significant human intervention or decision-making become automated. The monitoring of processes is an early area of focus for some operators – data is collected from sensors and computers installed on compressors or other equipment and transmitted to a central database, alerting companies when problems are detected. The inclusion of edge-level intelligence also allows for remote diagnostics and repair, reducing the need for employees to travel to worksites. The ultimate vision of automation in the oilfield is an unmanned field. Premier Oil’s Solan Oilfield Project is located in the North Sea, and has partnered with Emerson to provide automation solutions. The offshore platform is equipped with an integrated control and safety system. The system is controlled remotely via satellite link from an onshore control room – workers only visit the system for monthly inspection and maintenance, greatly reducing operating costs.

Impact Across Upstream O&G Players will be Diverse

The digital oilfield has the potential to transform the O&G ecosystem, with differing impact across players adopting the digital oilfield.

IOCs

The Digital Oilfield allows IOCs to offer a new dimension of differentiation in an increasingly competitive industry, as well as enabling the potential for significant operational improvements. While the scale of IOCs may make implementation of digital oilfield solutions more difficult, its impact may also be accelerated due to sheer amount of data that is available for analysis. Operational improvements may increase the amount of economically viable projects or increase the lifespan of existing projects, something that would benefit IOCs greatly given current commodity pricing. IOCs regard the digital oilfield as an important evolution in the industry as they try to maintain a competitive advantage in a shifting competitive landscape, as evidenced by investment in digital technologies by a number of major IOCs including Shell, ExxonMobil, Chevron and BP.

NOCs

NOCs, may view the digital oilfield as an opportunity to take back power from IOCs, as the application of digital oilfield may give them a unique opportunity to disrupt the position of IOCs and mitigate the advantage that IOCs have of accumulated technological and operational expertise. Additionally, NOCs may be able to bridge the knowledge and skill gap between them and IOCs. By working with oilfield services companies, traditional tech giants, and emerging start-ups, NOCs could potentially challenge IOCs for a portion or the entirety of oilfield development. However, while such opportunities exist, NOCs may find it harder to achieve a fully integrated oilfield due to the bureaucratic culture and hierarchical organizational structure that is deeply embedded within most NOCs. In addition, governments are typically more sensitive to the cybersecurity risks than private sector, and will take extreme precaution with their sensitive, proprietary information. Even among NOCs, there is a bifurcation between established and advanced NOCs that may adopt digital oilfield technologies more rapidly vis-à-vis less sophisticated NOCs that will be sluggish in adoption. For example, since 2010, Saudi Aramco, a more sophisticated NOC, has commenced 4 major projects related to digital oilfields – real-time drilling, real-time geosteering, intelligent fields and event solution optimization – to take advantage of digital oilfield opportunities in upstream O&G.

Independents

Independent operators face the challenge of scaling up without increasing organizational complexity – they are typically less hierarchical and bureaucratic than traditional IOCs, but scaling growth in the company may be difficult without adding these elements. Adopting an integrated operating model through the use of digital technologies can help independents build up scale without dramatically increasing organizational complexity, allowing independents to augment competitive advantages against large IOCs and compete more effectively against them. In addition, independent operators are typically less mature and may not be operationally optimized – digital oilfield technologies can help these operators become more efficient and catch up with competitors.

Oilfield Services Companies

Oilfield services companies will likely be the leaders in digital oilfield implementation / adoption. Their role in the value chain allows them to serve IOCs, NOCs, and independents, allowing them to focus on operational improvements without having to worry about new competitive threats. Their large scale affords them a large trove of data to extract insights from and market conditions will force emphasis on operational efficiency. However, OFS companies should be aware of competition from IOCs in digital oilfield applications, as IOCs will likely work to provide the same types of digital services to their clients, taking away some portion of their potential clients. As a result, OFS companies may invest more heavily in the space to maintain advantages over competitors and top-tier operators.

Looking Ahead

These solutions are only viable if there is a steady stream of accurate data from oilfield assets to aggregate and analyze. While most oilfield assets have not been equipped with IoT and data gathering capabilities, there has been robust development of the software and data analytics engines necessary to generate insights. This should reduce the time between enabling oilfield assets with data collection and beginning operational optimization using this data.

With substantial interest from oil operators of all types and a clear value proposition, the oilfield looks to finally become digitized in the near future. However, there are still several issues players should keep an eye on as the ecosystem develops:

- Technology drivers and adoption cycles – will technology adoption by a few major operators lead to most other oil operators quickly following, thereby catalyzing adoption, or will the migration be more gradual?

- Business model evolution – the implementation of digital oilfield solutions enables IOCs and oilfield services companies to offer a more diverse set of capabilities – there may be a shift towards outcome-based models as the oilfield becomes more quantifiable

- Investment in the Digital Oilfield – while many operators are pursuing organic initiatives, a robust startup scene may make it more attractive for some to look for inorganic options to address gaps in capabilities, delivery, resources, and/or technology